February 3, 2026

·

read time

FEED outcomes confirm low-cost, strong economics

Tees Valley Lithium FEED Outcomes Confirm Low-Cost, Finance-Ready Project

Tees Valley Lithium has announced the outcomes of its Front-End Engineering Design (FEED) programme for its proposed lithium hydroxide refinery in Teesside, confirming a technically defined, economically robust project positioned to progress towards Final Investment Decision.

The FEED outcomes confirm that Tees Valley Lithium is designed as a low-cost, merchant lithium refinery, capable of supplying battery-grade lithium chemicals to the rapidly growing European electric vehicle and battery market.

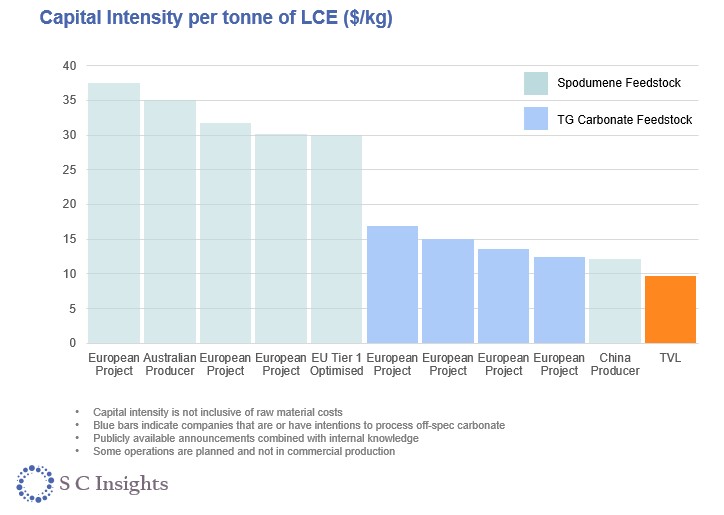

Low-cost position confirmed by independent analysis

The FEED study confirms total capital expenditure of approximately US$243 million, placing Tees Valley Lithium among the lowest-capex lithium refining projects globally and, according to independent benchmarking by SC Insights, the lowest in Europe on a like-for-like basis.

Estimated operating costs are approximately US$33 million per annum, benefiting from Teesside’s established industrial cluster, integrated infrastructure, and the use of proven processing technology. Independent benchmarking positions the project at the low end of the global operating cost curve for lithium refining.

Strong, predictable project economics

The combination of low capital intensity and low operating costs supports forecast EBITDA of approximately US$66 million per annum. Importantly, EBITDA is driven by processing margins rather than exposure to lithium price volatility. This results in more predictable, infrastructure-style cash generation.

Built to serve Europe’s battery demand

The proposed facility is designed to produce 25,000 tonnes per annum of battery-grade lithium hydroxide monohydrate, a critical material for electric vehicle batteries. European battery manufacturing capacity is forecast to exceed 900 GWh per annum by 2030 (according to public announcements), equating to approximately 720,000 tonnes per annum of lithium carbonate equivalent demand (0.8kg LCE per KWh).

Against this backdrop, Tees Valley Lithium’s initial production capacity represents less than 3% of projected European demand, highlighting both the scale of the market opportunity and the potential for phased expansion.

Major de-risking milestone achieved

The FEED outcomes define the project’s technical design, capital framework, site ownership, and execution strategy to a level that supports financing and progression towards Final Investment Decision. This represents a significant de-risking milestone in the development of the project.

Tees Valley Lithium has secured ownership of its Teesside industrial site, providing long-term control, cost certainty, and a stable platform for future expansion. The facility has been engineered using a modular, plug-and-play design philosophy to support efficient and controlled construction delivery.

Commercial validation in place

The project is further underpinned by a binding offtake agreement covering up to 40% of initial production capacity with a wholly owned subsidiary of Glencore Plc, one of the world’s leading commodity companies. The offtake agreement provides early commercial validation and supports revenue visibility as the project advances towards financing and FID.

Next steps

With the FEED programme complete to a level supporting financing and execution planning, Tees Valley Lithium is now progressing project financing, contractor engagement, and the remaining regulatory and permitting activities in parallel, with the objective of advancing the project to Final Investment Decision.

Tees Valley Lithium is being developed as a cornerstone piece of infrastructure for the UK and Europe’s battery supply chain, combining Teesside’s industrial heritage with a globally competitive cost structure and a clear focus on deliverability.

.svg)

.png)